The SpaceX IPO Launch Sequence

Retail wants access. Its real advantage is not having a deadline.

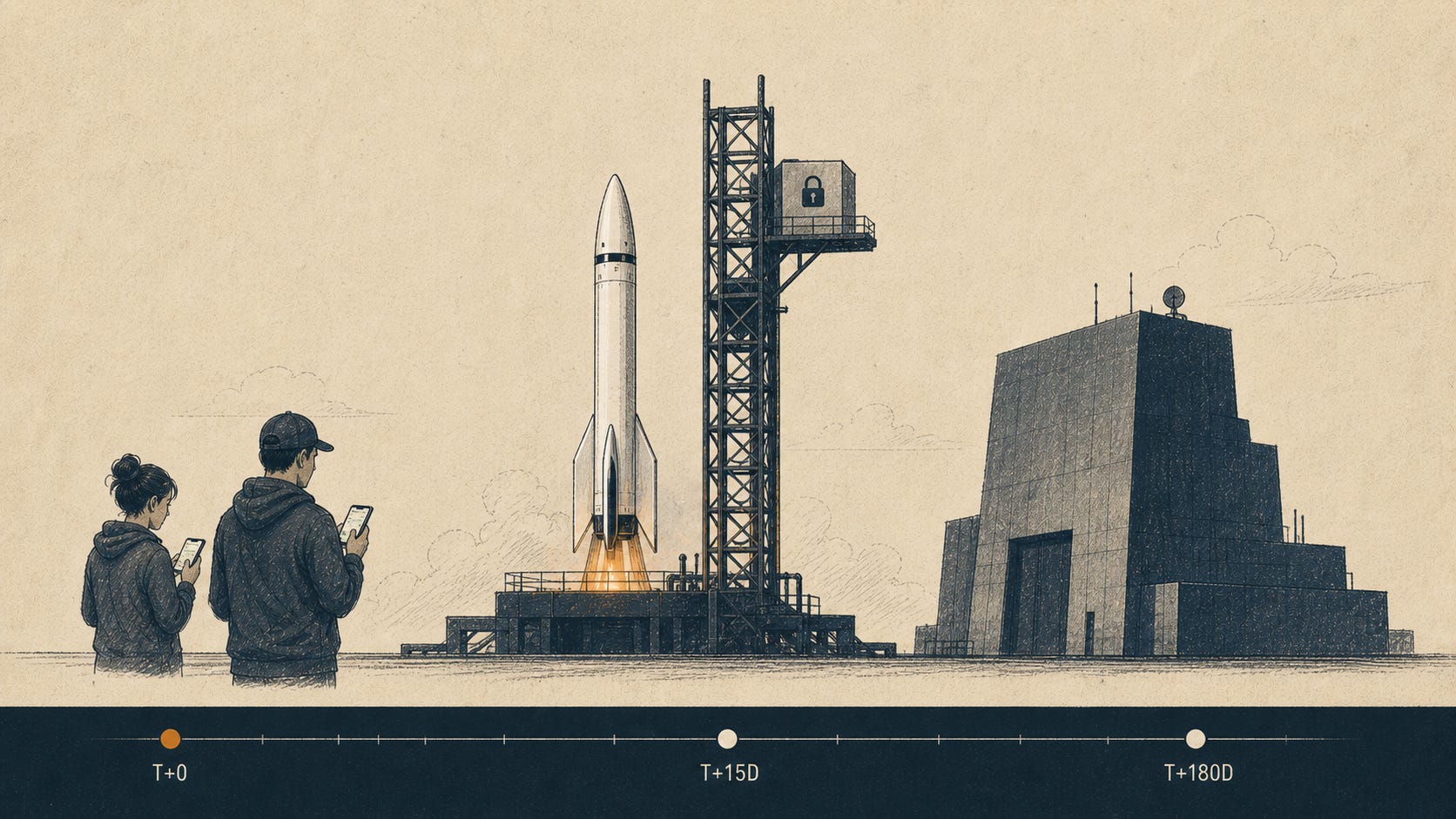

Most people will look at the SpaceX IPO and ask: should I buy it?

That is the wrong first question.

The better question is: where am I in the launch sequence?

First, retail and institutions. Then possible Nasdaq-100 benchmark demand after 15 trading days. Later, insider supply becomes easier to sell.

That is the high-level version of this post. SpaceX can be an extraordinary company. Starlink can be one of the best satellite communications businesses ever built. Rockets can be the moat that makes Starlink hard to copy. But none of that means the first public trade is automatically a good retail entry point.

Retail investors usually think their edge is access. Can I get shares? Can I buy on day one? Can I get in before everyone else?

In this IPO, the useful edge is the opposite.

Retail does not have to join the timetable. Unlike an index fund, it has the option to watch the sequence play out first.

This article is general information only and is not financial advice. It does not take into account your objectives, financial situation, needs, or risk profile. If you are making investment decisions in New Zealand, consider getting advice from a licensed financial advice provider.

Disclosure: I am a Starlink customer, and I love the product. That makes me more sympathetic to the bull case, not less careful about the price.

This is also an experiment in using AI as a research analyst. In I Don't Consume the Internet Raw Anymore, I wrote about using AI to turn the firehose into something usable. In Who Becomes the Compiler?, I argued that judgement becomes more important when execution gets cheaper.

This is that idea applied to a stock filing. I asked AI to read the S-1, pull out the business segments, explain the lock-up rules, check the index rules, and map the bull and bear cases.

The useful output was not a price target. It was a sequence of incentives.

What are you buying?

The simple version is that SpaceX is three things in one: Starlink is the business, rockets are the moat, and AI is the bill.

That is true today. The bull case is that all three eventually become one system.

Starlink is the part I can most easily understand wanting to own. SpaceX's Connectivity segment, mainly Starlink, generated $11.387 billion of revenue in 2025 and $7.168 billion of Segment Adjusted EBITDA. By 31 March 2026, Starlink had about 10.3 million subscribers across 164 countries, territories, and other markets.

That is a real business. People pay for it. Governments pay for it. Ships, planes, farms, rural households, and mobile networks can use it. As a customer, I can say the product is genuinely useful.

The rocket business is different. It launched 170 times in 2025 and delivered 2,213 metric tonnes to orbit. That is extraordinary operationally, but I do not think of rockets as a clean standalone cash machine. I think of them as the system that lets Starlink exist at scale.

Then there is AI. The AI segment includes xAI, Grok, X, AI compute, and the larger story about terrestrial and orbital compute. In 2025, it generated $3.201 billion of revenue, posted a $6.355 billion operating loss, and consumed $12.727 billion of capital expenditure.

Bulls will argue that compute, data, distribution, and orbital infrastructure belong in the same long-term system. Maybe. But the public story will sound simple: rockets, Starlink, Mars, Elon. The actual investment package is more complicated. It includes a large, loss-making AI option investors are being asked to fund.

The fair version of the AI bear case is not that Grok is useless. It is that SpaceX's AI segment is not yet a proven platform business in the way OpenAI, Anthropic, or Google are. Ramp's AI Index shows business spend concentrated around OpenAI and Anthropic. SpaceX's AI segment is still trying to prove it belongs in that commercial category.

Why launch day will be wild

Day one will be about scarcity and emotion.

Reuters reported that SpaceX CFO Bret Johnsen told bankers retail would be a much larger part of the offering than usual, with retail inclusion described as intentional because long-time supporters of SpaceX and Elon Musk should be recognised. The S-1 also says certain Class A shares are expected to be offered to retail investors through platforms including Charles Schwab, Fidelity, Robinhood, SoFi, and E*TRADE by Morgan Stanley.

That is better than a system where only institutions get the IPO price. But allocation and after-market buying are not the same thing. If a retail investor gets shares at the offer price, that is one thing. If the stock opens up 30%, 50%, or more, you are no longer buying the IPO. You are buying from someone who got the IPO.

That distinction matters in New Zealand too. Local retail buyers using familiar brokerage apps, including Sharesies, are unlikely to be getting IPO allocation. For most Kiwi buyers, the "IPO" will really mean the after-market. By the time the buy button appears locally, the offer-price allocation has already happened, Nasdaq has opened, and the first wave of price discovery is underway.

The hype has an obvious local accelerant because New Zealand already has a space-stock reference point in Rocket Lab. Rocket Lab is not SpaceX. It is smaller, already public, and has its own losses, valuation questions, and volatility. But it has taught a cohort of Kiwi retail investors that space can work as a public-market narrative.

Rocket Lab's Q1 2026 results reported record quarterly revenue of $200.3 million and a $2.2 billion backlog. Sharesies data also showed Rocket Lab made up 9% of activity in the final week of June 2025 as investors bought and took profits.

That does not mean SpaceX will be a good buy at any price. It means the story will already feel familiar, and familiarity is not safety.

Why day 15 matters

The other unusual part is the Nasdaq-100 rule change.

Nasdaq changed its Nasdaq-100 methodology before SpaceX filed publicly. Under the updated methodology, a newly listed company can get fast entry into the Nasdaq-100 if its full market capitalisation ranks inside the top 40 current index constituents and it meets the other eligibility tests.

For an IPO, Nasdaq typically evaluates the company after its seventh trading day, announces inclusion after the tenth trading day, and adds it after 15 trading days.

That does not mean SpaceX is automatically added. But if it qualifies and Nasdaq admits it, funds that track the Nasdaq-100 need benchmark exposure. They are not buying because they love Starship or Starlink. They are buying because the benchmark changed.

That is why the 15-day window matters. Benchmark demand may not wait politely until day 15. Once the market believes inclusion is likely, hedge funds and index-arbitrage desks can start buying ahead of the official rebalance. By the time passive funds need clean benchmark exposure, some of that demand may already be priced in.

The money also has to come from somewhere. A fund like QQQ says in its SEC prospectus that it uses full replication, meaning it invests in Nasdaq-100 securities in proportion to their index weights. Funds can implement this through trading, ETF baskets, cash flows, derivatives, or transition management. The economic pressure is real, but it is not one giant mandatory buy order.

SpaceX could qualify based on full market capitalisation, but that does not mean the whole headline valuation becomes index demand. Nasdaq's FAQ explains that low-float companies are capped for weighting purposes. Its example of a $1 trillion company with a 6% float would have had about a 1% Nasdaq-100 weight as of March 2026, implying about $6 billion of buying from $600 billion of tracking assets. That is Nasdaq's scale illustration, not my SpaceX forecast.

There is a quiet New Zealand version of this too. If you are in KiwiSaver, you may already be exposed to this machinery without thinking of yourself as a SpaceX investor.

The important detail is that not all passive funds follow the same index. A Nasdaq-100 KiwiSaver option would be closest to the day-15 story. A US 500-style fund would only get SpaceX if S&P adds it to the S&P 500. A broad developed-market fund would depend on its own index provider, screens, and rebalance rules. Many KiwiSaver funds may have no direct SpaceX exposure at all.

This is the broader point. Passive investing does not mean no one is making decisions. It means many of the decisions have been moved into the index methodology, fund mandate, and implementation rules. If those rules eventually include SpaceX, a passive investor may receive exposure without making a separate SpaceX decision.

Brokerage apps are the visible retail channel. KiwiSaver is the quieter background channel. A Kiwi could buy SpaceX on day one because the app makes it feel accessible, then later receive a small indirect exposure through passive retirement savings, depending on the fund they are in.

Possible index inclusion can create early demand, but it is not free money. Everyone can see the same countdown. Traders can front-run it. Passive funds can end up paying a worse price. After inclusion, the obvious benchmark buyer may already be gone.

What happens after the excitement?

After the early demand story, the supply story begins.

The simple answer people give is "there is a 180-day lock-up." The SpaceX filing is more complicated. Musk and certain significant investors are subject to a separate 366-day lock-up, while many other holders have a 180-day framework with staged early-release provisions.

Some shares can become transferable after Q2 results. Additional tranches can release at 70, 90, 105, 120, and 135 days after the offering. More can release after Q3 results, and the remaining early-release eligible shares can transfer at 180 days.

The exact share counts are not final in the preliminary prospectus, and unlocks create potential supply rather than guaranteed selling. They are not sell orders. They are dates when potential supply becomes easier to trade.

The point is simple enough: this is not one clean cliff. It is a supply staircase.

That is the part I would want to understand before chasing the launch. The early period may be about finding enough shares for people who want to buy. The later period may be about finding enough buyers for shares that can finally be sold.

That is why the wrong first question is "Do I believe in SpaceX?"

The better question is: where am I in the launch sequence?

Before the benchmark demand, after the benchmark demand, or just before insider supply gets easier to sell?

That does not tell anyone whether to buy. It tells you what game you are in.

Retail's advantage is not speed. It is not access. It is not having the same deadline.

I'm Ben Lynch. I write about founders, AI, and what happens next from New Zealand. Say hello at ben@thinkdorepeat.ai.

If you're new here, Start Here is the best place to begin.

If you own passive funds and had never read the index methodology before, this is probably worth forwarding to someone else who hasn't either.